BNPL App Development Costs in 2025: Key Features, Process & Factors Affecting Price

Nikunj Patel

Associate Director of Software Engineering

December 7, 2025

Key Takeaways

- BNPL is no longer a “nice-to-have” feature; it’s a trillion-dollar shift in how people shop and how businesses grow.

- A successful BNPL app must combine user convenience, merchant control, compliance, and fraud protection.

- The real cost of building a BNPL app lies in balancing consumer convenience, merchant control, and regulatory compliance on a scalable foundation.

- With the right partner like Zymr, businesses can build future-ready BNPL platforms that scale globally and deliver measurable ROI.

Think about the last time you shopped online. Chances are, you noticed an option to “Buy Now, Pay Later” (BNPL) right at checkout. What started as a “nice-to-have” feature is now transforming into a global financial movement. In fact, McKinsey predicts that BNPL transactions could exceed $1 trillion by 2030, as more people choose interest-free installments over traditional credit cards. And it’s not just consumers driving the trend.

Why is this happening? Modern shoppers, especially Millennials and Gen Z, expect flexibility without the heavy baggage of credit cards. They want to spread payments, shop responsibly, and enjoy instant gratification. For businesses, BNPL doesn’t just add convenience; it can lift average order values by up to 40% and reduce cart abandonment, directly impacting the bottom line.

But here’s the catch: building a BNPL app isn’t just about creating a payment option. The cost of developing a BNPL app depends on dozens of factors, everything from features and integrations to security, compliance, and long-term scalability. It’s a complex process that requires more than coding skills.

This is where partners like Zymr come in. We’ve helped fintechs design and build secure platforms for financial risk management, payment fraud detection, and secure software development. Our approach ensures that BNPL apps are functional, resilient, scalable, and ready for real-world growth.

In this blog, we’ll unpack everything you need to know about the factors that shape BNPL app development costs, must-have features, cost estimates, and how to maximize ROI. Whether you’re a startup testing the waters or an enterprise scaling globally, this guide will help you understand what it really takes to build a seamless BNPL app.

Key Factors Affecting BNPL App Development Costs

One of the first questions business leaders ask when exploring BNPL app development is: “How much will it cost us to build?” The honest answer is- it depends. Think of it like building a house. A cozy one-bedroom apartment costs far less than a custom-designed villa with smart security, solar panels, and a rooftop pool. The same logic applies to BNPL apps: the more features, complexity, and safeguards you need, the higher the investment.

Here are some of the most significant factors that shape the overall cost:

1. Scope and Complexity

A basic BNPL app that just splits payments is quick and relatively affordable to build. But if you want advanced features like real-time credit scoring, fraud detection, merchant dashboards, and multi-currency support, you’re looking at more development time and cost.

2. Regulatory and Security Layers

Handling financial data means there’s no room for shortcuts. Compliance with standards like GDPR and PCI-DSS isn’t optional; it’s essential. Meeting these requirements adds effort to development and builds trust with users and regulators.

3. Technology Choices

The tech stack you choose, whether cloud-native microservices or more traditional architectures, will impact how scalable and secure your app is in the future. It’s like choosing between building a house with brick or lightweight materials.

- User Experience (UX) Design

People won’t use a financial app they don’t trust. And trust often starts with design. A clear repayment schedule, smooth onboarding, and intuitive dashboards require thoughtful UX, not just a few pretty screens. - Third-Party Integrations

BNPL apps don’t live in isolation. They must connect with payment gateways, merchant systems, fraud detection tools, and credit bureaus. Each integration adds time and complexity, but it’s what makes the app truly useful. - Team Expertise and Location

An experienced fintech engineering team may cost more than a generalist developer, but their knowledge can save you from expensive mistakes later. In addition, where your team is located, whether Silicon Valley, Eastern Europe, or Asia, can significantly influence costs. - Ongoing Support

Launching the app isn’t the finish line; it’s the starting point. Regular updates, bug fixes, compliance checks, and new feature rollouts all add to the total cost of ownership.

So, the “cost” of a BNPL app isn’t just about lines of code. It balances user trust, compliance, scalability, and business goals.

At Zymr, we help companies make these decisions strategically. With expertise in secure software development and DevOps in fintech, we ensure that you invest wisely and build a safe, scalable, and future-ready BNPL platform.

From Costs to Capabilities: Why Features Matter

Now that we’ve looked at the significant factors influencing BNPL app development costs, the next big question is: “What exactly should my app include?” After all, it’s not just about how much you spend, but what you get for that investment.

The features you choose will shape the user experience, the trust your app builds, and ultimately the success of your BNPL offering. Some features, like secure payment options and transparent repayment schedules, are essential, while others, such as advanced analytics or loyalty programs, can set your app apart in a crowded market.

Let’s explore the must-have features every BNPL app needs to deliver value to customers and merchants.

Essential Features of a BNPL App

When you think about what makes a BNPL app successful, it really comes down to the features that make life easier for customers while protecting businesses. Here are the essentials, explained simply:

- Simple Sign-Up & Profile Management

Nobody enjoys filling out endless forms. A BNPL app should let users quickly create an account with the necessary details while still securely verifying their identity. The easier it is to get started, the more likely people will use it. - Flexible Payment Options

This is the core of BNPL: letting users split their purchases into smaller payments instead of paying everything upfront. The ability to choose the number of installments or set payment dates makes the app feel convenient and trustworthy. - Real-Time Credit Checks & Risk Assessment

Behind the scenes, the app must decide whether a customer is financially reliable before approving the “pay later” option. This protects businesses from unpaid bills and keeps the system fair, without making users wait for lengthy approvals. - Secure Payment Gateway Integration

Once a purchase is made, the money must move safely between banks, merchants, and users. Integrating with reliable payment gateways ensures every transaction is fast, smooth, and secure. - Fraud Detection & Security Layers

Since BNPL deals with money, fraud is always a concern. Features like data encryption, tokenization, and AI-based fraud monitoring act like invisible guards, catching suspicious activity before it becomes a problem. - Transparent Transaction History

Users should never be left wondering how much they owe or when payments are due. A clear dashboard showing purchases, repayment dates, and receipts helps build confidence and keeps users in control of their finances. - Push Notifications & Alerts

Gentle reminders before a payment is due or confirmations after a successful transaction help users stay on track and avoid late fees. This simple feature makes a big difference in customer satisfaction. - Merchant & Admin Dashboards

BNPL isn’t only for shoppers; merchants and admins need their own view too. These dashboards give businesses insights into transactions, settlements, and customer behavior while helping them manage risks and comply with regulations.

In short, these features are the foundation of a BNPL app that people can trust and enjoy using. Without them, businesses risk creating a tool that confuses customers or exposes them to unnecessary risks.

Essential Features of a BNPL App

Consumer-Side Features (for Shoppers)

These are the features that make BNPL apps easy, safe, and convenient for everyday users:

- Quick Sign-Up & Easy Onboarding

Shoppers don’t want long forms or endless steps. A BNPL app should let them create an account in minutes, with simple ID checks that feel effortless but keep the process secure. - Flexible Payment Plans

People use BNPL mainly because they can split their purchases into smaller payments instead of paying them all at once. Giving users choices (like paying in 3, 6, or 12 installments) makes them feel more in control. - Instant Approval & Credit Checks

Instead of waiting days like with a bank loan, BNPL apps quickly check users' ability to pay back and approve them in real time. This makes shopping smooth and keeps buyers from walking away at checkout. - Secure Payments

Users need to know that their money and personal details are safe. The app works with trusted payment gateways and adds security measures to ensure every transaction happens smoothly and securely. - Clear Transaction History

No one likes surprises when it comes to money. A simple dashboard showing all past purchases, upcoming payments, and due dates helps users stay organized and avoid confusion. - Smart Notifications

Gentle reminders before a payment is due or alerts when a payment goes through keep users on track. It’s like having a helpful assistant that makes sure they never miss a deadline.

Merchant-Side Features (for Businesses/Admins)

These features give businesses the tools they need to manage BNPL services while protecting themselves from risks:

- Merchant Dashboard

A single panel allows businesses to see all activity, such as who’s buying, how much is being spent, and when payments are due. This makes it easier to stay on top of sales. - Risk & Fraud Detection

Just like banks, BNPL providers need protection from fraud. Built-in systems that flag unusual behavior, such as someone suddenly making very large purchases, help keep businesses safe from losses. - Settlement Management

Even if customers pay in installments, merchants don’t want to wait months for their money. BNPL apps ensure businesses receive payments quickly while handling user collection in the background. - Customer Insights & Analytics

Beyond selling, businesses can learn about shopping habits, such as which products people prefer, how often they repay on time, and what keeps them returning. This data helps them make smarter decisions. - Compliance & Reporting Tools

Since BNPL deals with financial transactions, businesses must follow strict rules (like GDPR or PCI-DSS). Built-in tools automatically generate reports or track compliance, making this process less painful. - Admin Controls

Merchants need flexibility, whether adjusting repayment terms, handling disputes, or setting spending limits. Admin features give them control without requiring developers to be involved every time.

In short, consumers gain flexibility and peace of mind, while merchants gain transparency, security, and data-driven insights. When the app covers these bases, both sides benefit.

At Zymr, we’ve helped fintechs strike this balance, building risk management platforms and fraud detection systems that empower end-users and businesses.

Essential Integrations for a BNPL App

BNPL apps don’t work in isolation—they connect with other systems to handle payments, prevent fraud, and keep everything running smoothly. Here’s how the integrations break down for consumers and merchants:

Consumer-Side Integrations (for Shoppers)

- Payment Gateways

These pipes move money securely between the app, banks, and merchants. Without them, payments can’t happen. Think of them as the digital equivalent of a secure cash register. - Credit Check & Verification Services

Before approving a “pay later” option, the app quickly checks if a user is creditworthy. Integrating with credit bureaus or alternative data providers makes this process instant and hassle-free. - Identity Verification (KYC)

BNPL apps often integrate Know Your Customer (KYC) checks to prevent misuse. This confirms that the user is who they claim to be without making sign-up feel like applying for a mortgage. - Mobile Wallets & Bank APIs

Linking with Apple Pay, Google Pay, or direct bank APIs makes paying installments as easy as a

Merchant-Side Integrations (for Businesses/Admins)

- E-commerce Platforms

To offer BNPL at checkout, the app must connect with popular platforms like Shopify, WooCommerce, or Magento. This makes it simple for merchants to enable BNPL without a complex setup. - Fraud Detection Engines

Advanced tools that analyze behavior and flag suspicious activity (like multiple high-value purchases in seconds). These protect businesses from revenue loss. - Accounting & Settlement Systems

BNPL providers must ensure merchants get paid on time. Integrating with accounting software and settlement systems automates payouts, keeping cash flow predictable. - Analytics & Reporting Tools

Businesses need more than just transactions; they need insights. Integrations with analytics platforms help track repayment trends, customer preferences, and compliance metrics. - Regulatory Compliance Systems

To meet rules like GDPR or PCI-DSS, BNPL apps often integrate compliance frameworks that automatically generate reports and track sensitive data securely.

In simple terms, consumer-side integrations make the app easy and safe, while merchant-side integrations keep the business running securely and profitably.

At Zymr, we’ve implemented similar integrations in fintech solutions, from secure payment systems to cloud security testing platforms, ensuring that shoppers and merchants enjoy a seamless experience.

Buy Now Pay Later App Development in 6 Steps

Building a BNPL app isn’t just about coding a payment option; it’s about creating a secure, compliant, and user-friendly financial product. Here’s a straightforward look at the six main steps in the journey:

- Research & Planning

Every great app starts with a blueprint. This phase is about understanding your target audience (shoppers, merchants, or both), defining the business model (interest-free, fee-based, or hybrid), and mapping out the features you want to include. A clear plan here saves costly rework later. - Design the User Experience (UI/UX)

Shoppers won’t stick around if the app feels confusing. This step focuses on creating a clean, intuitive interface- smooth onboarding, transparent repayment schedules, and easy-to-navigate dashboards. Good design builds trust and keeps users engaged. - Backend Development & Architecture

This is the engine room. Developers build the system that manages payments, runs real-time credit checks, handles fraud detection, and keeps user data safe. Choosing the right tech stack here is crucial for scalability and performance. - Integrations with External Systems

BNPL apps need to connect with many outside services- payment gateways, credit bureaus, e-commerce platforms, and fraud detection engines. Each integration adds critical functionality that makes the app usable in real-world scenarios. - Testing & Compliance Checks

Before going live, the app goes through rigorous quality assurance (QA). This includes performance testing, penetration testing, and ensuring compliance with regulations like GDPR and PCI-DSS. The goal is to catch issues early and protect both users and merchants. - Deployment & Post-Launch Support

Once everything checks out, the app is deployed to the market. But the work doesn’t stop there. Regular updates, security patches, feature enhancements, and user feedback loops are essential to keep the app relevant and secure over time.

At Zymr, we follow this exact process when building fintech platforms combining secure software development practices with DevOps in fintech to ensure apps launch quickly, stay compliant, and scale without disruption.

From Process to Price: Understanding the Costs

Now that we’ve walked through the step-by-step journey of building a BNPL app, the natural next question is: “How much does all of this cost?” The answer isn’t straightforward, because each step, whether it’s planning, design, integrations, or compliance, comes with its own price tag. Some apps are lean MVPs built for startups, while others are enterprise-grade platforms designed to scale globally. In the next section, we’ll break down the estimated cost ranges for BNPL app development so you can see what it takes to bring your vision to life.

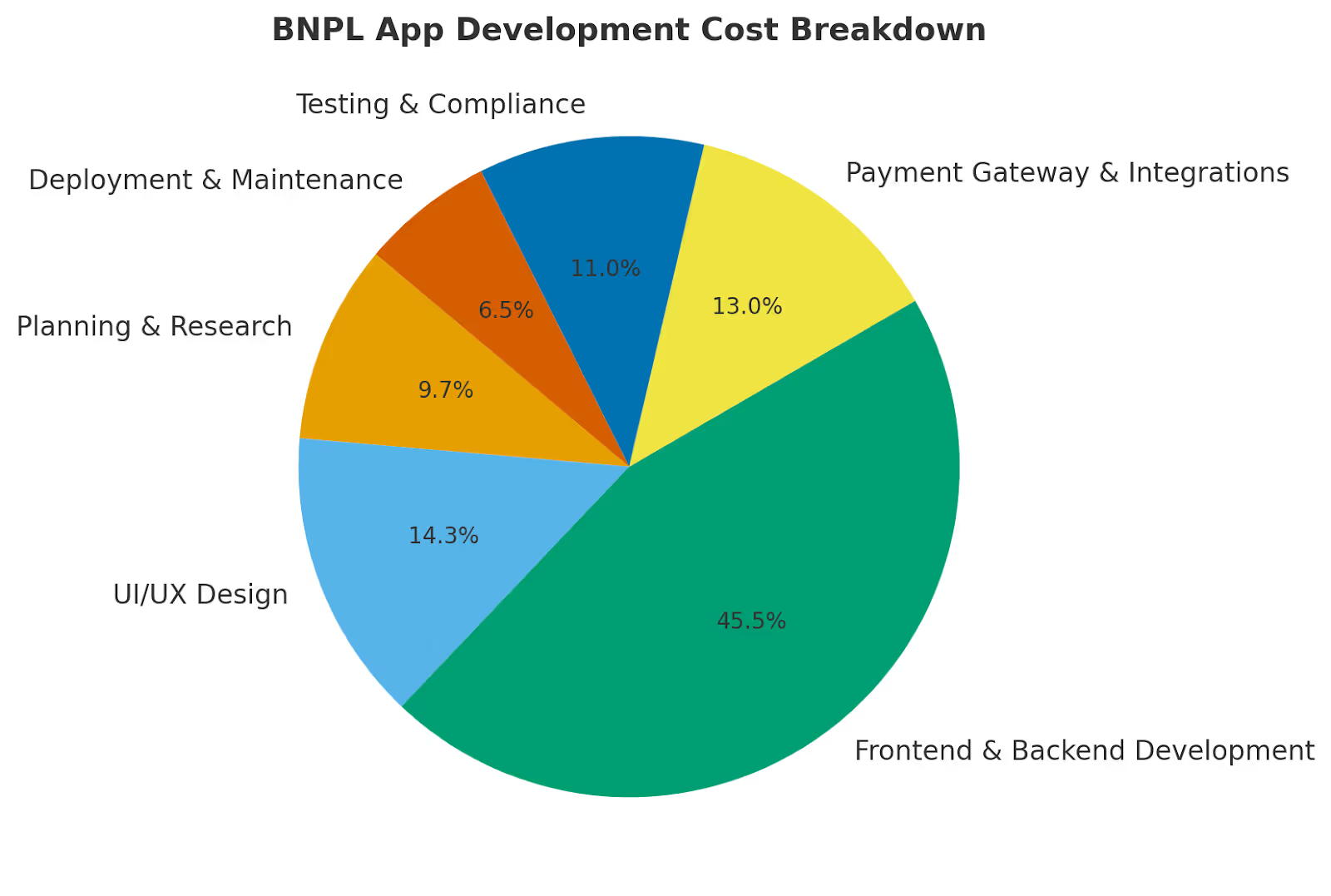

Estimated Cost Breakdown of BNPL App Development

The cost of building a BNPL app depends heavily on its complexity, features, and compliance needs. To give you a realistic idea, here’s a breakdown of what different types of builds usually cost:

Cost Components in Detail

While the overall cost of a BNPL app depends on its complexity, breaking it down into key components gives a clearer picture. Here’s what typically goes into the budget:

- 1. Planning & Research ($5K – $10K)

This is the blueprint stage, understanding your target users, compliance requirements, and deciding the business model (interest-free, fee-based, or hybrid). Skipping this step often leads to costly rework later, so it’s a small but essential upfront investment. - 2. UI/UX Design ($7K – $15K)

A BNPL app must inspire trust from the very first screen. Investing in clean, intuitive design, smooth onboarding, clear repayment schedules, and transparent dashboards, pays off in higher adoption and fewer user drop-offs. - 3. Frontend & Backend Development ($20K – $50K+)

This is the engine of the app. The backend handles credit checks, payment logic, and fraud detection, while the frontend makes everything accessible to users. The cost here varies widely based on features, architecture (monolith vs. microservices), and scalability needs. - 4. Payment Gateway & Integrations ($5K – $15K)

Integrating with trusted gateways (Stripe, PayPal, Adyen, etc.), e-commerce platforms, and third-party services like credit bureaus ensures the app can function in the real world. Each integration adds cost but is vital for seamless operation. - 5. Testing & Compliance Checks ($5K – $12K)

Since BNPL apps deal with sensitive financial data, rigorous testing is critical. This includes functional QA, performance tests, penetration testing, and compliance audits (e.g., PCI-DSS, GDPR). Cutting corners here risks app failures or legal penalties. - 6. Deployment & Maintenance ($3K – $7K per year)

Launching the app isn’t the finish line; it’s the starting point. Ongoing costs include cloud hosting, updates, bug fixes, security patches, and adapting to new regulations. Maintenance ensures the app remains reliable and competitive.

When budgeting for a BNPL app, it helps to see where the money actually goes. This breakdown highlights which areas take the largest share and why each is essential for building a secure, scalable platform.

Looking at the cost breakdown, it’s clear that the biggest share of a BNPL app budget goes into frontend and backend development, which makes sense since this is where payment logic, credit checks, and security layers are built. UI/UX design and third-party integrations also take a meaningful portion, as they directly shape how users and merchants interact with the app. Planning and research, while smaller in cost, are crucial for setting the right foundation. Testing, compliance, and ongoing maintenance may seem like smaller slices, but they’re the safeguards that keep the app secure, reliable, and legally sound long after launch.

Tips to Optimize BNPL App Development Costs

Building a BNPL app can feel like a big investment, but smart choices along the way can help you control costs while still delivering a secure and scalable product. Here are some proven ways to optimize:

- Start with an MVP (Minimum Viable Product)

Instead of trying to build everything at once, launch a lean version with only the must-have features like sign-up, payment splits, and a dashboard. This keeps initial costs down and lets you test the waters before committing to advanced features. - Use Pre-Built Components Where Possible

Many essential features like payment gateways, fraud detection, or ID verification, don’t need to be built from scratch. Leveraging reliable third-party APIs saves both time and money. - Prioritize Security Early On

It may sound counterintuitive, but investing in security from day one is cheaper than fixing compliance or fraud issues later. Building on solid secure software development practices prevents costly rework. - Choose the Right Tech Stack

Going cloud-native and modular means your app can grow without expensive rebuilds. A well-chosen stack ensures long-term savings by avoiding scalability bottlenecks. - Outsource Smartly

Hiring an experienced fintech engineering partner in cost-effective regions can give you top-notch quality without Silicon Valley price tags. What matters most is expertise in fintech, not just location. - Adopt Agile Development

Breaking the project into smaller sprints with continuous testing helps spot issues early, saves rework, and keeps the app aligned with business goals. - Plan for Maintenance Upfront

Don’t ignore the costs of updates, bug fixes, and compliance audits. Budgeting for ongoing support ensures stability and prevents surprise expenses later.

The key is not about cutting costs, but about spending wisely. By focusing on what matters most to users and merchants in the first release, you can control expenses while building a strong foundation for future growth.

Factors that Drive ROI for a BNPL App

Spending money to build a BNPL app only makes sense if it generates real returns. The good news? BNPL apps have multiple ways to create value, for both merchants and providers. Here are the main drivers of ROI:

- Higher Conversion Rates at Checkout

When shoppers see they can “buy now and pay later,” they’re far less likely to abandon their carts. This simple option can significantly increase completed purchases. - Increased Average Order Value (AOV)

Customers tend to spend more per transaction when payments are split into smaller amounts. For merchants, this means bigger baskets without extra marketing spend. - Customer Loyalty & Repeat Purchases

Offering BNPL creates a sense of flexibility and trust. Shoppers often return to businesses that give them convenient payment choices, which leads to recurring revenue. - Merchant Fees & Transaction Revenue

BNPL providers typically charge merchants a small percentage on each transaction (usually 1–3%). These fees add up quickly as transaction volumes grow. - Late Payment & Convenience Fees

While the core offering is often interest-free, providers can still earn from reasonable late fees or premium options for flexible repayment schedules. - Data-Driven Insights

BNPL platforms collect valuable data on consumer spending habits. This anonymized information can guide product decisions, enable targeted offers, and even open up new monetization opportunities. - Licensing the Platform

Some BNPL providers package their technology and offer it as a service to other businesses, creating an additional revenue stream.

The real ROI of a BNPL app isn’t just in revenue, it’s in long-term growth. Businesses gain loyal customers, higher sales, and actionable insights, while BNPL providers build recurring income and stronger market positioning.

How Zymr Can Help in Building Seamless BNPL Apps

Building a BNPL app isn’t just about putting together features; it’s about creating a secure, compliant, and scalable ecosystem that customers trust and merchants rely on. That’s where Zymr comes in.

Here’s how we make a difference:

- Security and Compliance First

With money and sensitive data at stake, BNPL apps must be bulletproof. Zymr brings expertise in software development practices, cloud security testing, and compliance with global standards like PCI-DSS and GDPR. We help you launch confidently, knowing your app can withstand audits, regulations, and cyber threats. - Proven Fintech Track Record

We’ve delivered solutions ranging from financial risk management platforms to payment fraud detection systems. This means we already understand the complexities of economic data, fraud risks, and transaction flows, and can apply that knowledge to your BNPL platform. - Cloud-Native, Scalable Architecture

BNPL isn’t just about today; it’s about tomorrow’s growth. Whether you are starting with an MVP (minimum viable product) or planning a global rollout, our DevOps in fintech approach makes sure that your app can scale smoothly, with continuous delivery, automated testing, and resilience built in. - End-to-End Partnership

We work alongside your team from design workshops to deployment to align technical decisions with business goals. Our consulting-led approach ensures you get a working app and a BNPL solution tailored to your strategy and market. - Faster Time-to-Market with Quality

With pre-built accelerators, Agile methodologies, and deep fintech expertise, we help you cut down development cycles without compromising security or user experience.

In short, Zymr doesn’t just build apps; we help fintech innovators launch trustworthy, future-ready BNPL platforms that win customers, earn loyalty, and deliver measurable ROI.

Conclusion

FAQs

How long does it take to develop a BNPL app?

>

It depends on complexity. A basic MVP with core features can be built in 2–3 months, while a mid-level app may take 4–6 months. Enterprise-grade BNPL platforms with advanced integrations and compliance can last 9–12 months.

Can startups build a BNPL app with a limited budget?

>

Yes. The best approach for startups is to begin with an MVP that covers must-have features like sign-up, payment splits, and a simple dashboard. This keeps initial costs manageable, allows quick market testing, and leaves room to add advanced features later.

How can I monetize a BNPL app?

>

BNPL providers usually earn through merchant transaction fees (1–3% per sale). Additional revenue can come from late payment fees, premium repayment options, data-driven insights, or even licensing the BNPL platform to other businesses.

What tech stack is best for BNPL app development?

>

There’s no one-size-fits-all, but popular choices include: Frontend: React Native, Flutter, or native iOS/Android for mobile apps Backend: Node.js, Java, .NET, or Python for secure, scalable services Database: PostgreSQL, MySQL, or MongoDB Cloud & DevOps: AWS, Azure, or GCP with CI/CD pipelines for resilience Security: Data encryption, tokenization, MFA, and compliance frameworks like PCI-DSS and GDPR

>

It depends on complexity. A basic MVP with core features can be built in 2–3 months, while a mid-level app may take 4–6 months. Enterprise-grade BNPL platforms with advanced integrations and compliance can last 9–12 months.

Have a specific concern bothering you?

Try our complimentary 2-week POV engagement

Our Latest Blogs

July 29, 2026

How to Build an Ambient Clinical Documentation Solution (AI Medical Scribes) - The 2026 Build Playbook

July 28, 2026

Building a Custom ML Pipeline: The 2026 Reference Architecture, Open-Source Building Blocks, and Decision Framework

July 27, 2026

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)